- Average House price is £357,750 (England & Wales), up 1.5% on December; annual increase is 7.7%

- West Midlands heads annual price growth at 12.0%

- Wales slips back after leading for six months

- South East climbs into second place with 10.3% rise

- North East edges along at 1.1%

Richard Sexton, director at e.surv, comments:

“Leading the way this month with the largest increase in annual house price growth is the West Midlands, up from 9.5% to 12.0%, pushing Wales from the top position in the league table which it had held for the last six months. In the West Midlands, “Detached” homes have seen the highest percentage increase followed by “Semi-detached” and “Terraced” properties.

“Elsewhere, the return to work for many, even on a part-time basis, has meant that many commuter belt towns have fared well this month. Property analysts have recently noted that in the South East, towns such as Guildford, Esher, Farnham and Horsham are experiencing a strong pick-up in demand.

“There remains a supply crunch in the UK market. The lack of desirable stock available on the market has not deterred those wanting to move but has thwarted their ability to do so. New buyer registrations have remained strong yet the types of properties in demand (those that offer the potential for home office space or have gardens) are in poorer supply delivering further price support. Adding further pressure is the lack of supply of new housing as developers seek to recover from the impacts of the pandemic on labour and materials and endeavour to meet the government’s expectations of contributing to the remedial costs of cladding.

“While, at first glance, all this might appear to stack up against borrowers, mortgage competition remains keen and attractive long-term fixed rates are available. Combined with potentially substantial lockdown savings, many borrowers still have the wherewithal and desire to invest in new homes as this data is showing.”

Commentary: John Tindale and Peter Williams, Acadata Senior Analysts

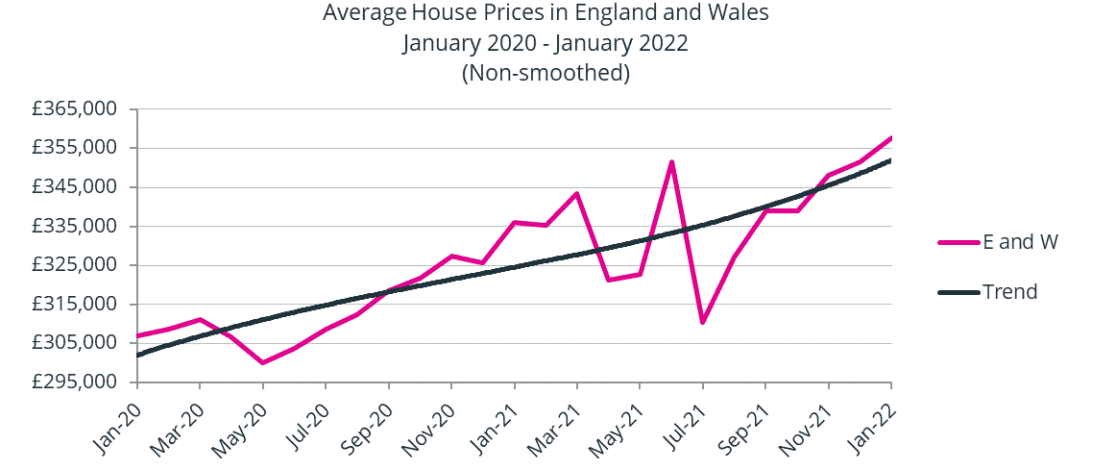

As we enter 2022, the Figure 1 graph shows an almost continuous rise in house prices since July 2021, albeit perhaps at just a slightly slower pace (i.e. less steep line). A key driver for this is the lack of stock coming onto the market, thus encouraging relatively strong competition for those properties that are put up for sale.

Although the temporary stamp duty incentives have long since ceased, there remains a relatively strong demand for properties still largely linked to the lifestyle changes brought about by the pandemic. Although the Government has abandoned its “Work from Home” recommendation, many organisations (and their employees) have fully embraced flexible working, suggesting that demand may well remain strong through this year – a matter we return to later.

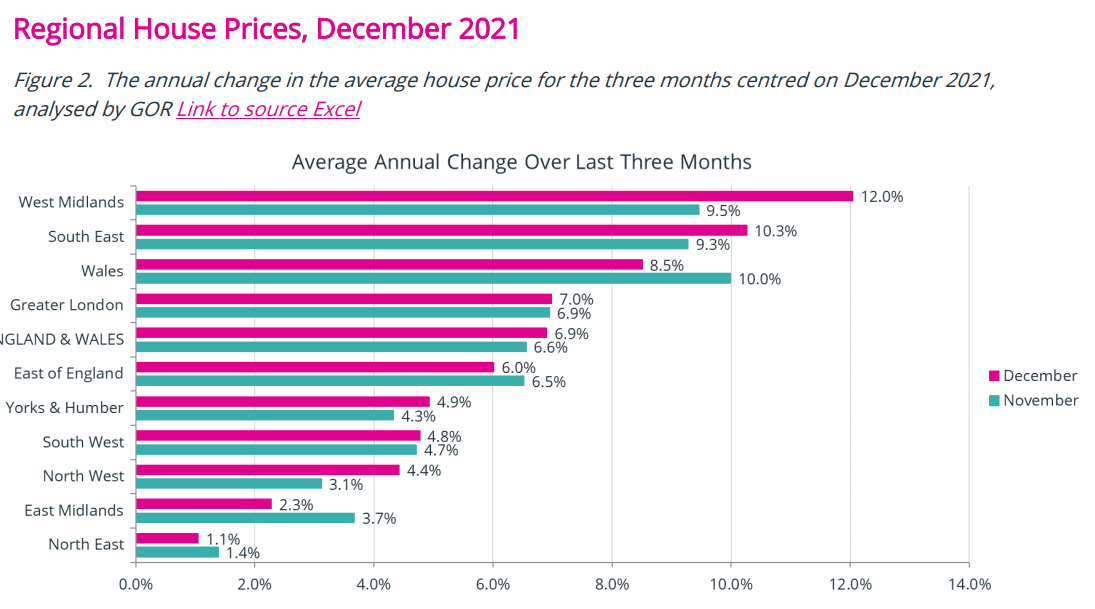

Figure 2 shows the percentage change in annual house prices on a regional basis in England and Wales for December, averaged over the three-month period of November and December 2021, and January 2022, compared to the same three months in 2020/21. It also shows the similarly-averaged figures for November 2021.

In general terms, six areas have seen an increase in their annual rate of growth, while four areas have seen a fall. The largest increase in rates, of +2.5%, was in the West Midlands, up from 9.5% to 12.0%, and thus pushing Wales from the top position in the league table – which it had held for the last six months. Seven of the eight unitary authority/metropolitan areas which constitute the West Midlands region set new record average price levels in December. The West Midlands is discussed in greater detail later in this report.

The area with the third highest increase in annual price growth was the South East, up from 9.3% in November to 10.3% in December, which puts the South East region in second place in the figure above. Property analysts have recently been noting that towns in the South East, such as Guildford, Esher, Farnham and Horsham, are experiencing a strong pick-up in demand, from purchasers who may need to commute into London once or twice per week.

The four areas which have seen price growth fall in December are Wales, down by 1.5% from last month’s 10.0%, the East Midlands (minus1.4%), the East of England (minus 0.5%) and the North East, down by 0.3%.

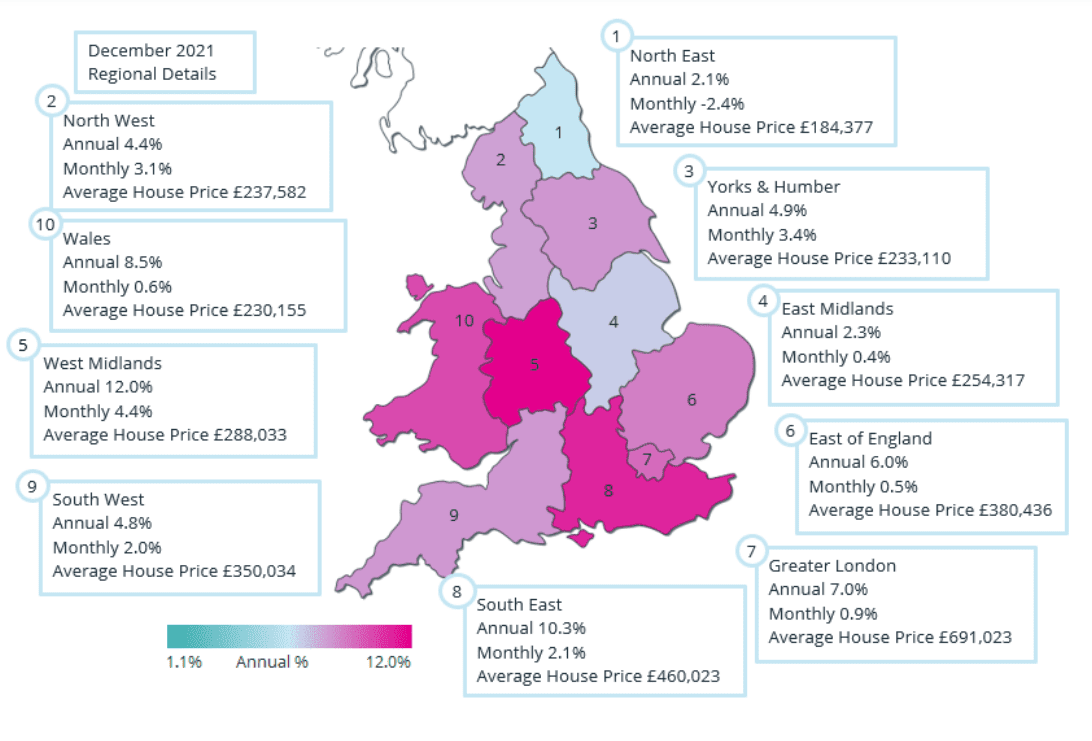

England and Wales Regional Heat Map for December 2021

These different trends are displayed below in the Regional Heat Map for December, though it is somewhat difficult to discern a specific spatial pattern. We can identify the two regions in blue on the east coast of England, indicating price growth below 2.5%. These areas are followed by a grouping of the North West, the South West and Yorkshire and the Humber, which lie in a growth range of 4.4% to 4.9% – but are located at almost opposite corners of England. There is then a grouping of the East of England, Greater London and Wales, with price growth ranging from 6.0% to 8.5.

Finally we have the two hot-spots of the South East and the West Midlands, where price growth is in double digits, of 10.3% and 12.0% respectively. While the so-called “race for space” may explain part of this, it is clear that other factors are at work.

The housing market in early 2022

As is evident from the above, the market is displaying considerable strength at the start of the year, despite being shorn of many of the incentives that carried it forward in 2021. Clearly, there are strong regional and country variations, but there is little evidence of the anticipated slowdown that some had suggested. Indeed, with the continuing shortage of supply – driven in part by the compounding effect of existing owners tending to buy their next home before selling their existing property – the shortage is exacerbated. Rising house prices have an inevitable impact on affordability, and this pressure will be added to should interest rates and general cost inflation rise through the year. At the same time, mortgage competition remains intense and borrowers have been able to lock in very attractive long-term fixed rates.

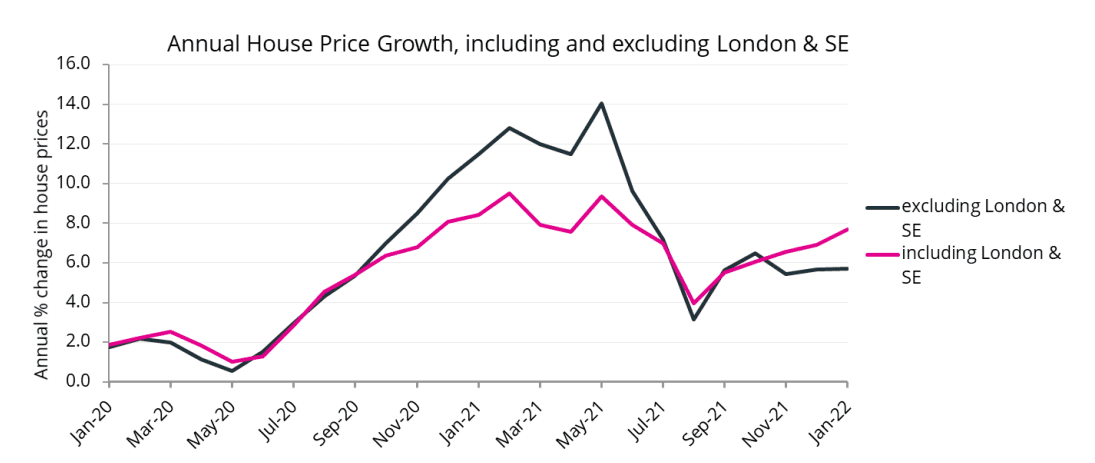

January – Annual Price Trends

Figure 3 shows the annual growth rate over the last two years for England and Wales, both including and excluding Greater London and the South East. As can be seen, the annual rates of house price growth between these two groupings were similar up to September 2020. However, as in previous periods, these two groupings have once again started to diverge. London and the South East held back the national rates from September 2020 to July 2021 (dates that roughly aligned with the period when the SDLT tax holiday was at its maximum in England, and the equivalent LTT holiday was also operational in Wales). Then over the period from July 2021 to September 2021, the LTT tax holiday in Wales ceased, and the SDLT holiday in England was at a much-reduced rate. During this time, the annual rates settled back to tracking one another. However, from October 2021, i.e. one month after the SDLT holiday in England had stopped, we can see that the two groupings again diverged, but this time with Greater London and the South East witnessing higher growth rates than elsewhere. Given the price differentials between regions and countries, a resurgent London and SE market does tend to drag national price indices upwards quite strongly, so it is clearly a factor to be borne in mind.

Transactions

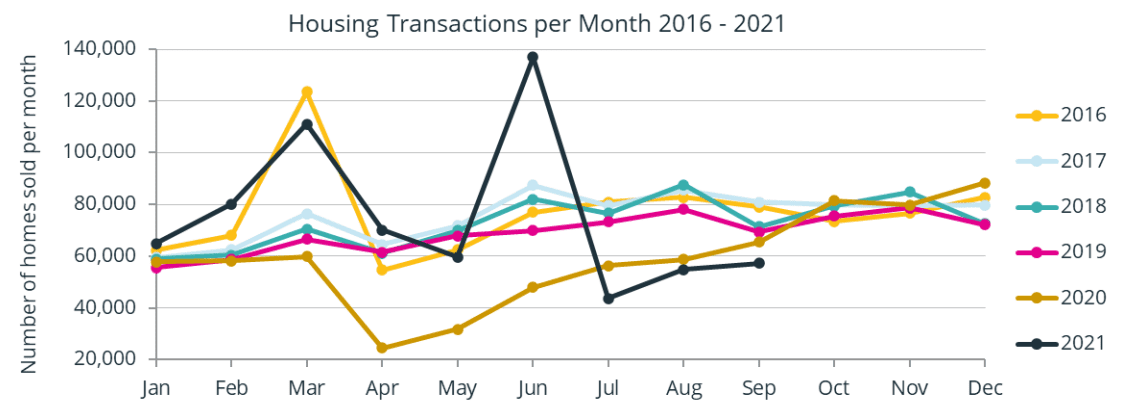

Figure 4 shows the number of domestic housing transactions per month recorded in England and Wales at the Land Registry for the period from January 2016 to September 2021. The named month is that of contract completion, i.e. the date when a property legally changes hands.

There are three conspicuous peaks on the graph, along with three associated troughs. The peaks are all stamp duty related events, taking place in March and June 2021 (in black) and March 2016 (in yellow). The March 2021 event was one month before the original date planned for Chancellor Sunak’s SDLT tax holiday to end – this termination date was in fact extended to 30 June 2021 at its full rate, and to 30 September 2021 at the reduced rate – but the announcement of its extension wasn’t made until 3 March 2021, and many purchasers already had plans to buy a property within the original timescale – hence the March 2021 spike. The second peak was in June 2021, the final date within which the full SDLT tax holiday was available under Sunak’s revised plans.

HMRC has published its estimates for domestic property sales in England and Wales for September 2021, suggesting that a further spike of 150,000 transactions took place in that month – but the Land Registry has to date only actually recorded 57,250 purchases for the month – watch this space as more data become available.

The other peak on the chart shows the 123,500 transactions that took place in March 2016 in England and Wales. This occurred one month ahead of the introduction of the 3% additional SDLT surcharge on second homes and buy-to-let properties, which caused a flurry of purchases in the month, so as to forestall the payment of the additional tax in April of that year.

Each spike in transactions tends to be followed by a dip in sales, reflecting the ability of buyers to bring forward their purchase into an earlier month.

For the record, the HMRC provisional estimates for the number of domestic housing transactions in England and Wales in October, November and December 2021 are 73,000, 89,200 and 100,600 respectively, although we should point out that we have found in the past that the HMRC transaction estimates are typically 30% higher than the final recorded Land Registry sales completions.

Help keep news FREE for our readers

Supporting your local community newspaper/online news outlet is crucial now more than ever. If you believe in independent journalism, then consider making a valuable contribution by making a one-time or monthly donation. We operate in rural areas where providing unbiased news can be challenging. Read More About Supporting The West Wales Chronicle

{kind=link}