- Short-term picture improves

- Housing market shrugs off September’s malaise

- Budget stamp duty measures will boost activity in coming months

- Southern England continues to hold back wider market recovery

- Average house price in October £354,822, up 0.2% on September, down 3.4% annually

Richard Sexton, Director at e.surv, comments:

“This month our data, which includes cash transactions, showed the average sale price of a home in England and Wales in October moved up to £354,800 – about £600 or 0.2% higher than in September – the first monthly rise in our index for six months and one that wiped out the fall of the previous month.

“Easing cost of living pressures, which have been helped this week by the cut in the Bank of England Base Rate, mean affordability will continue to improve as lenders’ standard variable rates follow suit.

“It remains to be seen if more cuts are in the pipeline. The markets suggest there will be more inflationary pressure ahead but for now, buyers should take advantage of the improved affordability – especially in light of the decision in the budget to return nil stamp duty thresholds back to their lower pre-September 2022 levels from April 2025.

The budget overall focussed on the long-term supply of housing and delivered nothing in terms of fiscal support for buyers in any market which is why interest rates will remain key over the coming months.”

In more detail –

October’s housing market

The average sale price of a home in England and Wales in October edged up to £354,800 – about £600 or 0.2% higher than in September.

On an annual basis, average prices in October remain about 3.4% lower than a year ago. This is a slight improvement on September, but still not materially different from where we began the year. Prices continue to be about £24,000 (more than 6%) below the previous peak reached in late 2022. Our index is based on both cash and mortgage based transactions, with the former making up to a third of transactions in some areas and often being the basis for stronger price negotiation especially given the somewhat volatile nature of the market in recent months.

Table 1. Average House Prices in England and Wales for the year to October 2024

|

Month |

Year |

Property Price |

Index |

Monthly % change |

Annual % change |

|

Oct |

2023 |

£367,361 |

374.1 |

-0.2 |

-3.1 |

|

Nov |

2023 |

£364,230 |

370.9 |

-0.9 |

-3.6 |

|

Dec |

2023 |

£363,843 |

370.5 |

-0.1 |

-3.6 |

|

Jan |

2024 |

£364,054 |

370.7 |

0.1 |

-3.5 |

|

Feb |

2024 |

£365,534 |

372.2 |

0.4 |

-3.1 |

|

Mar |

2024 |

£363,887 |

370.5 |

-0.5 |

-3.0 |

|

Apr |

2024 |

£364,164 |

370.8 |

0.1 |

-2.1 |

|

May |

2024 |

£363,539 |

370.2 |

-0.2 |

-1.8 |

|

Jun |

2024 |

£361,621 |

368.2 |

-0.5 |

-1.6 |

|

Jul |

2024 |

£357,205 |

363.7 |

-1.2 |

-2.6 |

|

Aug |

2024 |

£354,915 |

361.4 |

-0.6 |

-3.3 |

|

Sep |

2024 |

£354,235 |

360.7 |

-0.2 |

-3.7 |

|

Oct |

2024 |

£354,822 |

361.3 |

0.2 |

-3.4 |

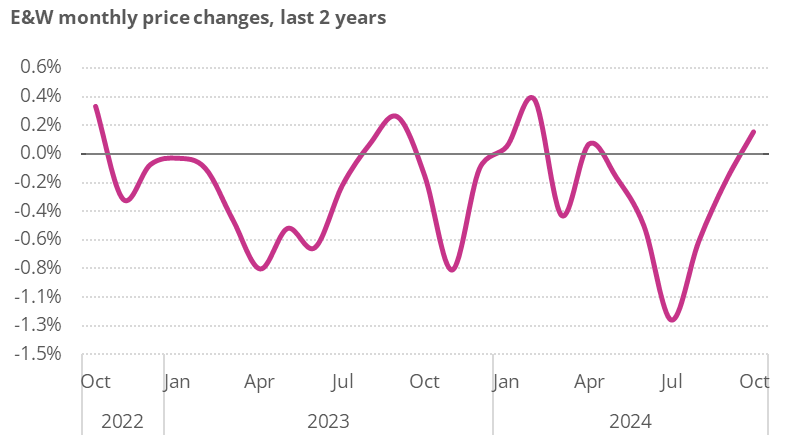

Figure 1. Downward pressure on prices subsides

That said, this was the first monthly rise in six months and largely unwound the decline seen a month earlier.

With a pick-up in demand over recent months on the back of easing cost-of-living pressures and more attractive mortgage pricing, we have seen a recovery in property sales. Monthly prices are currently on a modestly improving trajectory after oscillating around a more or less flat underling trend for much of the past two years (see Figure 1). This is a positive development given the Budget uncertainties of the past month or so, but we will have to see if this recovery story is sustained.

Although housing featured quite strongly in the Budget the announcements were more negative than positive.

Stamp Duty rises of 2% for landlords and second home-owners were perhaps predictable given the Government’s appetite to continue the policy stance of bearing down on those parts of the market.

Maybe more surprising was the decision to return nil SDLT thresholds back to their lower pre-September 2022 levels from April 2025 (as planned by the previous administration). This is likely to have a material impact on first-time buyers, who could face a stamp duty increase of up to £6,250 (or more if purchasing a home worth more than £500,000). This will probably double the proportion of FTBs paying SDLT and see a sharp rise in the number of households paying stamp duty in the Midlands, the North and South Western England. It will also land heavily on households looking to buy their first homes in the more expensive markets of London and the South East.

These threshold changes may boost Government revenue but they risk dampening demand. At the same time given the measure comes into play in April 2025 we now have a five-month window in which there is significant incentive to buy now! The upshot of all of this is that we should expect activity to pick up sharply in these next two quarters before probably slipping away in the spring of 2025.

It has also been suggested that the uncertainty in the run-up to the Budget also saw a big increase in older households drawing down on any tax free allowances from their pensions which in turn may boost the spending power of the Bank of Mum and Dad. Potentially we thus have a further stimulus to activity which itself might be supported by further Bank of England rate cuts.

Taken in the round this suggests we could see more transactions and more price pressures in the short term which might then taper off as we move through the year and into 2025. It is worth noting this is not how the Office for Budget Responsibility sees it. In its latest Economic and Fiscal Outlook it suggests prices and transactions will strengthen into 2025 as wages rise and interest rates fall. Clearly there are a lot of moving parts here.

The Budget is now behind us, Bank policy will probably become slightly clearer in the next week. But looking ahead we are now awaiting the publication of government’s long term housing strategy. We can expect to see this set out in greater detail the housing policies it will take forward not least for home ownership and private renting and the implications those might have for the market.

The English Regions and Wales

House prices in England and Wales continue to experience a slower and more subdued recovery than other parts of the UK.

In recent months all parts of England and Wales have shown a degree of short-term weakness, as Table 2 for the period to September shows.

Table 2. Average Prices in the English regions and Wales, September 2024

|

Geography |

Sep 2023 |

Aug 2024 |

Sep 2024 |

Monthly |

Annual |

|

East Midlands |

£276,612 |

£268,481 |

£269,074 |

0.2% |

-2.7% |

|

East of England |

£399,731 |

£386,211 |

£383,472 |

-0.7% |

-4.1% |

|

London |

£710,644 |

£676,184 |

£676,583 |

0.1% |

-4.8% |

|

North East |

£195,392 |

£194,053 |

£193,590 |

-0.2% |

-0.9% |

|

North West |

£249,872 |

£248,021 |

£247,837 |

-0.1% |

-0.8% |

|

South East |

£463,281 |

£441,522 |

£439,683 |

-0.4% |

-5.1% |

|

South West |

£370,285 |

£350,533 |

£350,234 |

-0.1% |

-5.4% |

|

West Midlands |

£285,888 |

£282,436 |

£280,311 |

-0.8% |

-2.0% |

|

Yorkshire and The Humber |

£243,802 |

£240,416 |

£242,084 |

0.7% |

-0.7% |

|

England |

£374,799 |

£361,334 |

£360,652 |

-0.2% |

-3.8% |

|

Wales |

£240,710 |

£235,931 |

£235,316 |

-0.3% |

-2.2% |

|

E&W |

£367,935 |

£354,915 |

£354,235 |

-0.2% |

-3.7% |

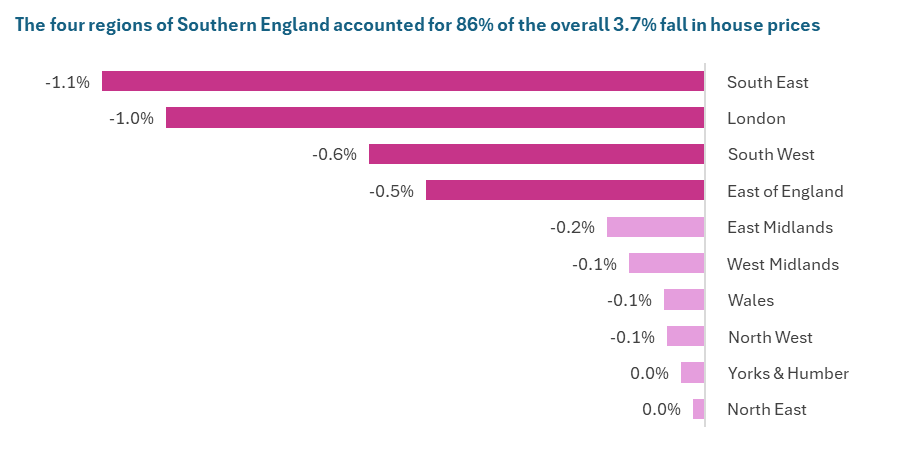

But the two-speed nature of the housing market has also been a significant contributory factor.

Figure 2. How areas contributed to England and Wales price growth, year to September 2024

The headline 3.4% year-on-year decrease in house prices seen across England and Wales in October would shrink to 2.6% if we exclude London and the South East.

We often default to looking at London and the South East because those regions account for about 30% of sales volumes and their elevated price levels add to their overall significance for England and Wales metrics. But it is worth noting that in recent months all the regions of southern England have acted to drag down the annual price changes for England and Wales (see Figure 2). Clearly this is not just a London and South East issue.

Figure 3 drills down a bit more and shows how prices in local authorities and counties across England and Wales have fared over the twelve months to September. As well as revealing a marked geographical divide, primarily between the northern and southern parts of England, the map highlights how uniformly subdued much of the South West region has been of late.

To the extent that the Budget and wider economic ramifications are felt differently across the regions as discussed earlier, this will clearly influence the pattern of recovery across regions and countries and how quickly the overall England and Wales picture improves.

Help keep news FREE for our readers

Supporting your local community newspaper/online news outlet is crucial now more than ever. If you believe in independent journalism, then consider making a valuable contribution by making a one-time or monthly donation. We operate in rural areas where providing unbiased news can be challenging. Read More About Supporting The West Wales Chronicle

{kind=link}