- Permanent extension of stamp duty threshold could provide fiscal surplus of £139m per year, generated by revenues based on higher consumption and increased housing market activity

- Approximately 37,000 more property transactions will take place each year

- Maintaining stamp duty threshold would provide boost to economy, mobility and downsizing

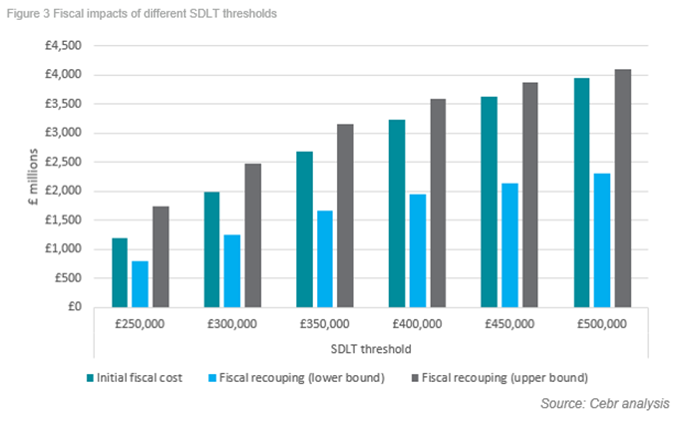

Extending the stamp duty holiday could be fiscally positive for the UK treasury, according to research commissioned by Kensington Mortgages. Retaining the threshold for paying Stamp Duty Land Tax (SDLT) at its current level of £500,000 would provide new tax revenues – generated by higher transaction volumes, increased property prices, household consumption, and housing market activity – ranging between £2.3 and £4.1 billion. According to analysis by the Centre for Economics and Business Research (Cebr), in the upper bound estimate this would lead to a fiscal surplus of £139 million.

Whilst maintaining the current SDLT threshold could generate a fiscal surplus at the upper bound level, the surplus increases as the threshold is lowered. If the threshold was lowered to £450,000, the net increase in tax revenues could rise to £247 million. Decreasing the threshold to £300,000 could lead to a surplus of £491 million per year.

Since July 2020, a stamp duty holiday has been in place for properties below £500,000 – which make up nearly 90% of transactions in England and Northern Ireland. The holiday is scheduled to end on 31st March 2021. This research indicates that the UK would derive significant socio-economic benefits from scrapping the temporary nature of the holiday.

Mark Arnold, CEO, Kensington Mortgages, comments:

“This research demonstrates what we all intuitively know – that the stamp duty holiday has been very positive for the economy at a critical time. The threshold level should be considered ripe for permanent reform. The upper bound estimates of our analysis suggest that the Treasury could have its cake and eat it, achieving a fiscal surplus whilst boosting the economy. It could unlock housing market activity and pay for 4,000 additional nurses in one fell swoop*.

“Furthermore, aside from updating the threshold to reflect real world house prices, the maintenance of the £500,000 threshold could address some structural problems with the UK housing market. It could lead to greater regional mobility – with ancillary trickle-down benefits – as well as also stimulate more downsizing, freeing up family homes and helping to address this vital stock shortage. We believe now is the time to be bold and keep the threshold at its current position, or at least consider amending it to a higher level than the previous £125,000.”

While the findings reveal that a permanent extension of the current SDLT, land and buildings (LBTT) and land transaction tax (LTT) holidays could cost the UK Treasury £3.9 billion per year, the below table summarises how it could recuperate between £2.3bn and £4.1bn.

|

|

Lower-bound |

Upper-bound |

|

Initial reduction in stamp duty receipts |

-£3.9 billion |

|

|

New stamp duty receipts from additional transactions |

£266 million |

|

|

New stamp duty receipts from higher prices |

£256 million |

|

|

Capital gains tax receipts associated with increase in property values |

£124 million |

|

|

Tax revenues associated with rise in consumption generated by reduced stamp duty burden |

£290 million |

£561 million |

|

Tax revenues associated with rise in consumption generated by increase in property values |

£1.4 billion |

£2.9 billion |

|

Taxes recouped |

£2.3 billion |

£4.1 billion |

Property transactions, collective wealth and household consumption will increase

Estimates from the Cebr suggest that the reduction in the rate of stamp duty would lead to 37,000 additional property transactions taking place each year, generating £266 million in annual revenues.

Future house prices could also be, on average, 1.3% higher. Moreover, the structure of SDLT means that the increase could be greater for higher-value properties, leading to a 1.9% increase in households’ collective property wealth. Higher property values could lead to SDLT, LBTT, and LTT receipts generating £256 million in additional revenues each year. Combined, higher property values and transaction numbers could generate £523 million of annual revenues to the Treasury.

With a significant share of households’ wealth contained within property, movements in house prices have a major effect on total levels of wealth in the UK. The analysis shows that the increase in house prices would lead to a £113 billion increase in households’ collective net wealth, driving an estimated 0.36% – 0.75% increase in household consumption.

Indirect fiscal impacts on capital gains tax

According to HMRC, between 2017 to 2018, the value of residential property transactions in which sellers were liable to capital gains tax (CGT) was £26.6 billion. The 1.9% increase in aggregate property wealth implies that the value of residential property transactions in which the seller is liable for CGT could also rise, by approximately £505 million each year.

For information on online loans click here: https://www.westwaleschronicle.co.uk/blog/2020/12/22/what-you-need-to…or-a-loan-online/

| [donate]

| Help keep news FREE for our readersSupporting your local community newspaper/online news outlet is crucial now more than ever. If you believe in independent journalism,then consider making a valuable contribution by making a one-time or monthly donation. We operate in rural areas where providing unbiased news can be challenging. |

{kind=link}