")

")

- Wales still enjoys the highest annual price growth rate at 11.2%

- Welsh price growth rate currently higher than all English regions

- The market is rebalancing after the partial ending of the tax holidays

Richard Sexton, director at e.surv, comments:

“House price growth is clearly in retreat in headline terms but there is little evidence of prices stagnating or falling. Indeed, regionally, there are substantial pockets of resistance to overall falls in house price growth.

“Our data shows that while some regions like the North East of England suffered their largest fall in the annual rate of growth (down by 6.3%) over the month, other areas like Wales fared much better. Indeed, Wales comfortably out-performed the rest of the country – having the smallest fall in price growth from 12.2% down to 11.2%. The Land Transaction Tax holiday came to an end at the end of June – but the tax savings available in Wales were not as large as in England (£2,450 in Wales vs £15,000 in England). This is we think a key reason potentially why the fall in prices in Wales has not been as significant as in England over the past few months. Wales therefore stands out as having the highest annual rate of price growth at 11.2%.

“In terms of property types, it’s worth noting too that, while the pandemic drove a race for space the price of flats in September staged a small recovery with the largest gains in flat prices being seen in Prime Central London and in Hammersmith and Fulham.

“On September’s data, there is little evidence that home buyers are being spooked by the end of the furlough scheme. Data from government points to a resilient job market that will further underpin buyer and lender confidence.”

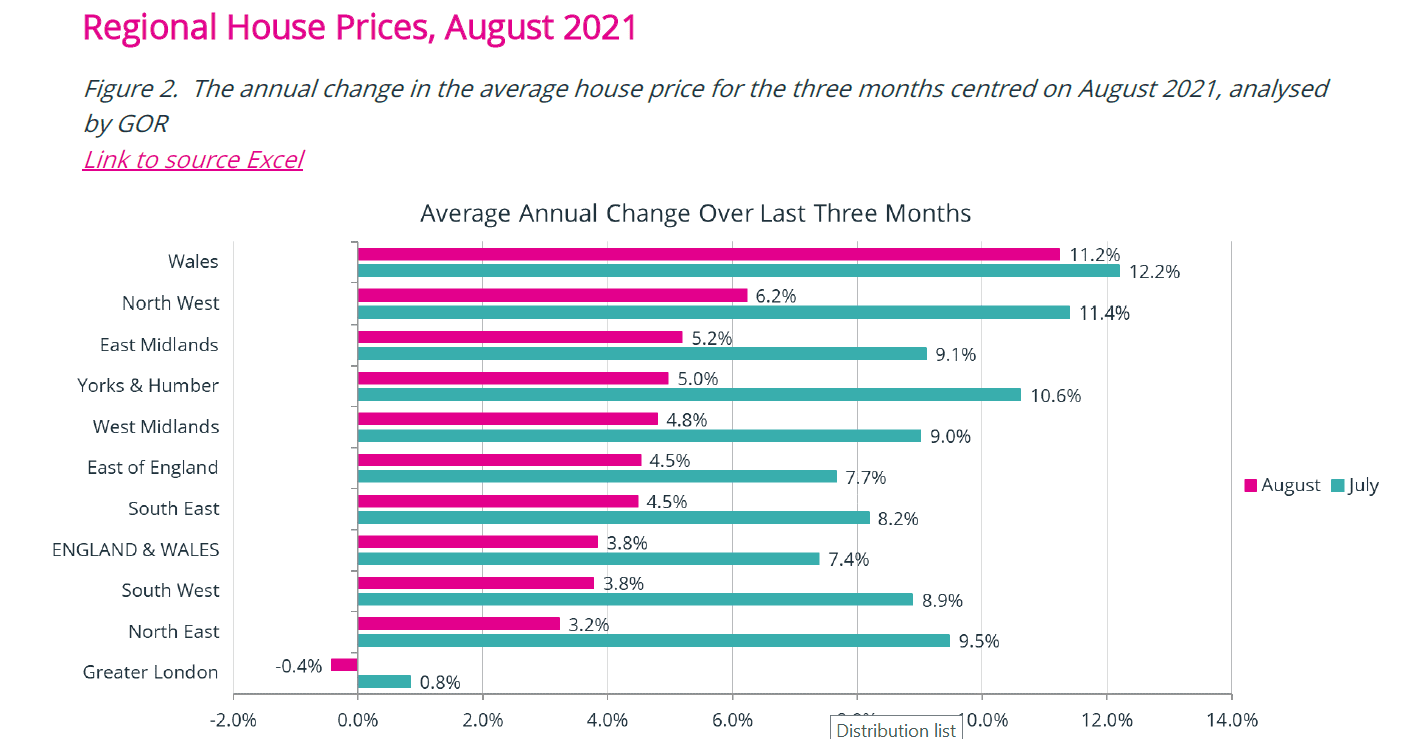

Figure 2 shows the percentage change in annual house prices on a regional basis for August, averaged over the three-month period of July, August and September 2021, compared to the same three months in 2020. It also shows the similarly-averaged figures from July.

In general terms, all areas – except for Wales at the top of the bar chart and Greater London at the bottom – have seen their annual rates of growth halve over the three months, being a consequence of the ending of the Stamp duty holiday for high value properties in June, since when the housing market in England has been rebalancing.

The largest fall in the annual rate of growth was in the North East, down by 6.3%, from 9.5% to 3.2% over the month. The North East was followed by Yorkshire and the Humber, down by 5.6% from 10.6% to 5.0% over the period. In fact, 79 of the 87 unitary authorities in England, excluding London Boroughs, or 91%, saw prices fall in the month.

Wales had the smallest fall in price growth in the month, from 12.2% down to 11.2%. The LTT tax holiday in Wales terminated at the end of June – but the tax savings available in Wales were not as large as in England (£2,450 in Wales vs £15,000 in England), which is potentially why the fall in prices in Wales has not been as significant as in England over the past few months.

In Greater London, 23 of the 33 boroughs, or 70%, saw prices fall in the month. Interestingly, 7 of the 10 boroughs with price increases in the month were in the top 10 boroughs by value, suggesting a price recovery in Prime Central London, at odds with the remainder of the Greater London area. Last month we were reporting that estate agents were seeing an increase in lettings and purchases by foreign nationals, as a result of the easing in travel restrictions and the start of a new university year. It looks as though these factors are working through the system and are being converted into property sales.

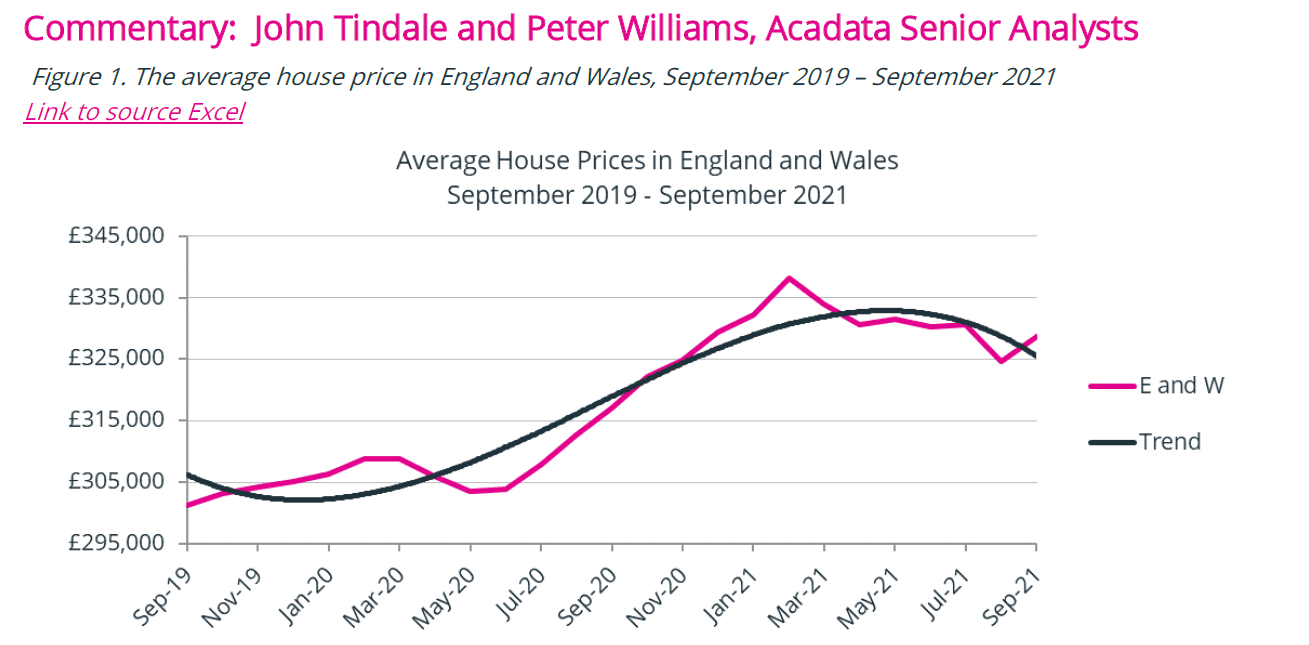

The market may have begun to settle on a new normality after two turbulent years – Figure 1 shows the path of the average house price in England and Wales over that period. House prices initially fell at the start of the pandemic in March 2020, but recovered three months later. This was in part due to the stamp duty holiday, introduced from 8 July 2020, and in part due to the lifestyle changes associated with working from home. The result was a significant shift in housing preferences to larger properties – with space for home working – rather than commuting to places of work.

Competition for large premises became prevalent, with prices rising as a consequence. Prices peaked in February/March 2021, coinciding with the scheduled date for the ending of the stamp duty holiday, although this date was subsequently extended to June in Wales, and to September in England, albeit at a reduced rate. The end-June date also caused a flurry of housing transactions and resulted in a smaller second peak in prices as can be seen on the graph.

Annual and Monthly Price Trends

The average price of all completed sales funded by both mortgages and cash grew at an annual rate of 3.6% in September. This is just 0.2% lower than the rate of 3.8% recorded in August, but is a reduction of 5.1% from the 8.7% growth in prices seen in June.

The slowing in price growth since June almost certainly relates to the ending of the first stage of the Stamp Duty holiday in England, along with the complete withdrawal of the Land Transaction tax holiday in Wales.

The influence of the SDLT tax holiday on England’s housing market is possibly best demonstrated by considering the number of transactions that took place over the period from June to August 2021. In June 2021, HMRC estimated that 190,760 residential sales took place in England and 8,060 in Wales. These levels of sales are double those usual in an average month. The much-reduced figures for July and August were 64,980 and 87,860 in England and 4,560 and 5,080 in Wales.

This pattern of sales volumes is often seen in the period surrounding the termination of such temporary tax holidays. In those situations, there is typically a spike in sales as the tax holiday deadline draws to its close, followed by a month – or two – when sales fall below their usual levels due to purchases having been brought forward into earlier months to take advantage of the tax savings, with transaction levels thereafter often returning to their more normal levels.

House prices also tend to follow a distinctive pattern during such periods, with higher average prices being seen in the last month of tax savings. This can then be followed by one or two months of low average prices, due to the likelihood that the purchase of higher-valued properties will have been brought forward to take advantage of the tax holiday. The consequence is that there can be fewer of them following the tax deadline, and lower-value homes could then weigh more heavily on price indices until the market rebalances. This has certainly been the case over the summer months in England and Wales.

The big question is, of course, what happens next? The tax holiday conferred individual advantage, but it also led to a wider market re-pricing, leading some households to pay more to buy their home. It is in essence a zero-sum outcome, and even the Exchequer has also done well out of it in terms of total tax revenue. Looking forward, it seems that the momentum in the market is far from spent and there doesn’t seem to be any sense of an imminent downturn.

Help keep news FREE for our readers

Supporting your local community newspaper/online news outlet is crucial now more than ever. If you believe in independent journalism, then consider making a valuable contribution by making a one-time or monthly donation. We operate in rural areas where providing unbiased news can be challenging. Read More About Supporting The West Wales Chronicle

{kind=link}