- The higher increase in rate reflects the low annual comparison points in July and August 2021

- Eight regions record growth increases of more than 10.0%

- London continues to have lowest price growth of all ten GOR areas

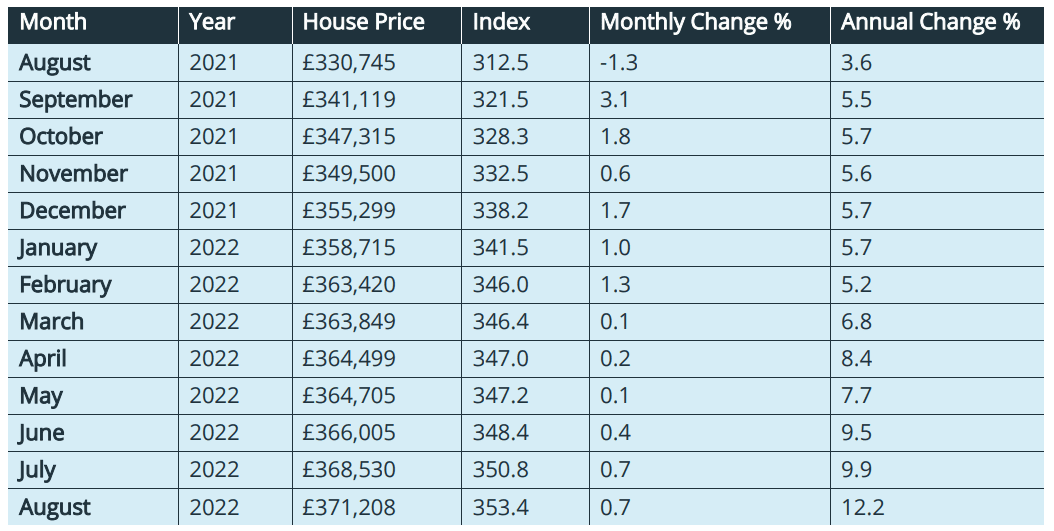

- Average house price now £371,208, up 0.7% on July

Richard Sexton, director at e.surv, comments:

“Despite recent anecdotal comments to the contrary, objectively at this time, our data records a resilient UK housing market – largely due to the continuing lack of supply of desirable stock and continued demand for it. There are some considerations to bear in mind. It is likely that, with the current extended completion times in the market, many of the transactions reported were agreed four or five months ago. Therefore, while the headlines show that the market remains resilient, we should acknowledge that some of the current affordability issues facing homeowners may not be reflected in the data yet. It remains to be seen what effect that has on subsequent data and we should also consider the potential positive impact of any new support to address the cost-of-living crisis from the new Government. Home-buying is a market built on sentiment and what happens next will fundamentally affect that.

“For this month, it is worth recognising that, notwithstanding the pressure already in the market, all ten GOR areas have experienced rising prices over the last twelve months, with nine of the ten areas setting new record average house prices in July 2022. Annual price growth has increased across England and Wales to 12.2%.

“As work habits continue to evolve and people settle into new ways of living and working, this continues to impact what people buy. We think the hybrid method of working from home for most of the week, is driving a revived interest in flats in the central areas of cities like London, which of course changes the mix of properties and values reflected in the index. How this plays out over time remains to be seen as many large companies have publicly already reverted to full-time office work.”

Table 1. Average House Prices in England and Wales for the period August 2021 – August 2022

Commentary: John Tindale and Peter Williams, Acadata Senior Analysts

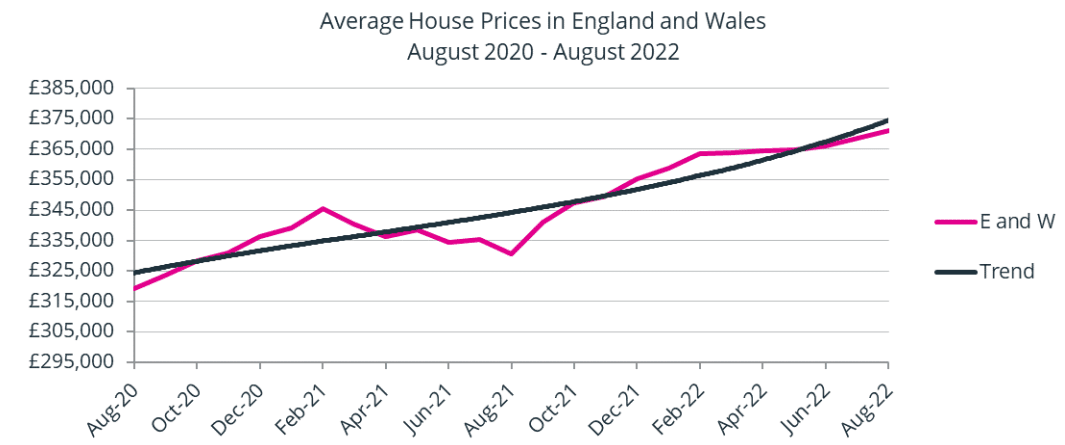

Figure 1. The average house price in England and Wales, smoothed, August 2020 – August 2022

The seemingly remorseless rise in house prices continues, with increases having occurred in each of the last twelve months. The average price paid for a home in England and Wales in August 2022 was £371,208, up by some £2,675, or 0.7%, on the revised average price paid in July. This underlines the continuing strength of the market and its ongoing ability to confound analysts.

From the start of the pandemic in March 2020 to the end of July 2022, the average house price has increased by some £53,800, or 17.1%, which contrasts with the increase in consumer price inflation (including housing – CPIH) of 11.6% over the same period. Property prices have thus risen in real terms.

As Figure 1 above shows, our HPI continues to record growth in the average house price throughout the first eight months of 2022, with a small upswing in the monthly rates from June 2022. Unlike most other price indices, Acadata uses residential price data from the Land Registry, which includes all mortgaged and cash sales across England and Wales

The housing market in August 2022

The RICS Residential Market survey for July showed that new buyer enquiries continued to decline, new instructions were stagnant and stock levels of homes for sale were at an all-time low. Prices were still rising, but the rate was moderating. Somewhat dated mortgage approval data also shows that the number of mortgages approved has been falling over the last few months – as have transactions (subject of course to the caveats re the data we list below) – but of course with a shortage of homes on the market, prices have still remained strong.

As noted earlier, the market has proved to be more resilient than many expected as measured by house prices, and in part due to limited stock and enhanced demand. Interest rate rises are now filtering through in mortgage pricing. Some 80% of borrowers are on 2- and 5-year fixed rates, but when they terminate, new loans will be more expensive. House price indices are starting to point towards lower monthly nominal price changes, and the question is whether that trend will gather momentum.

This is reflected in the Treasury’s comparison of independent forecasts. These forecasts for Q4 2022 range from +12.2 per cent in house prices to -1.5 per cent, highlighting the wide divergence of views that exist. The median was + 6.7 per cent, whilst OBR had projected + 4.3 per cent.

Projections for 2023 reveal a narrower range from + 3.5 per cent to – 4.0 per cent (median +1.3: OBR + 0.8), and again a divergence of views. Some clearly expect a significant slowing in the market, and given the rise in CPI to over 10 per cent – in real terms this represents falls in house prices.

Although mortgage arrears and possessions remain low, the current macro-economic context is likely to lead to more households slipping behind. UK Finance reported slight rises in early arrears in Q2 compared to Q1, but the numbers are low by historic standards.

Stretched affordability is widespread, and is no longer a feature of just London and the South East. Setting aside rising house prices and mortgage costs, the costs of renting have surged, reducing the capacity of some households to save a deposit (ever bigger to compensate for rising costs).

Reports of buyers exercising more caution in terms of the prices they are willing to pay suggests the market is starting to adjust to new circumstances, and we must now wait to see how such patterns are then reflected in prices. For the moment it is largely business as usual.

Average Annual Regional House Prices

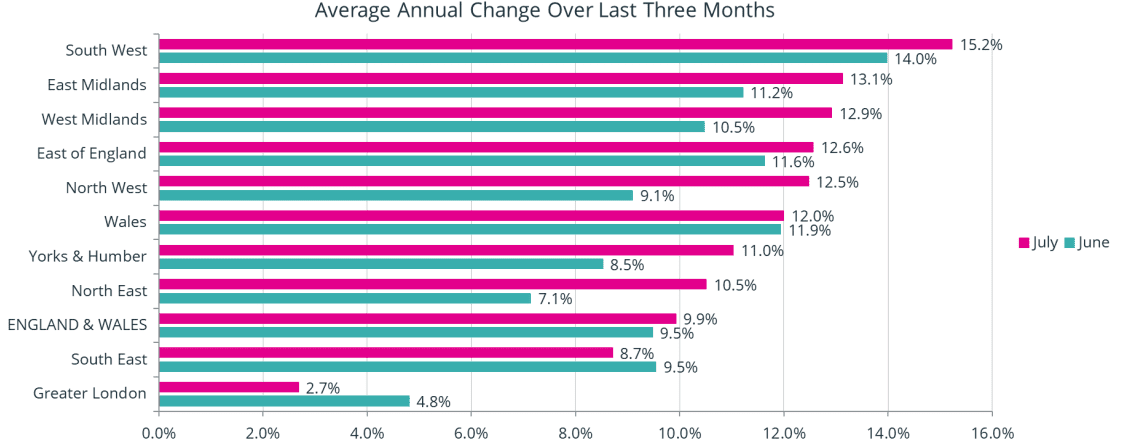

Figure 2. The annual change in the average house price for the three months from June 2022 to August 2022, analysed by GOR

Figure 2 shows the percentage change in annual house prices on a regional basis in England, and for Wales, averaged over the three-month period of June to August 2022, compared to the same three months in 2021. These figures are produced on a rolling three-month basis to smooth out minor changes in price, with Figure 2 showing the similarly averaged figures from one month earlier. All ten GOR areas have experienced rising prices over the last twelve months, with nine of the ten areas setting new record average house prices in July 2022. The one exception is Greater London, where prices are £12,650 below their peak. We look in more detail at the change in London prices later in this report.

All ten GOR areas have experienced rising prices over the last twelve months, with nine of the ten areas setting new record average house prices in July 2022. The one exception is Greater London, where prices are £12,650 below their peak. We look in more detail at the change in London prices later in this report.

Figure 2 above is showing some remarkably high levels of house price inflation in the July 2022 growth rates, with eight of the ten GOR areas seeing price rises in excess of 10%. There are perhaps two rarely observed factors that need to be considered when analysing these figures. Firstly, there is the fact that twelve months earlier, in July and August 2021, average house prices were lower than usual, since anyone buying a higher-priced property would have tried to purchase it in June 2021, when the tax savings, especially in England – unlike Wales – were at their most generous. Consequently, there was a dearth of higher-valued properties being purchased in July and August, which resulted in average prices falling in those two months. The base points for measuring house price gains were consequently low, which has had the effect of increasing the annual rate of growth recorded this year.

Secondly, as Rightmove and others continue to advise, on average it is taking four and a half months to complete a sales transaction. This means that a sale which the Land Registry records as having taken place at the end of July might actually have been agreed in principle half-way through March, with the conveyancing process rumbling on during the intervening months. And back in March, only three of the six interest rate rises which have been introduced by the Bank of England over the last year had taken place, and the Ukrainian war would only just have started (the Russian invasion commenced on February 24th).

The conditions then were considerably different from those that apply today, and with the four-and-a half-month delay in recording the sale, the current published data is perhaps obscuring the changing circumstances around current house prices.

The South West remains top in July in terms of house price growth (Figure 2) at 15.2%. Within that region, Bath and North East Somerset has led the way in the South West, with annual price growth of 24.2%. This is also the highest rate of all 113 Unitary Authorities across England and Wales. Bath is followed by Bournemouth, Christchurch and Poole as being the second highest Unitary Authority in England and Wales at 22.1%, which in turn in the South West is followed by Devon at 19%. Interestingly, Cornwall has only seen 7.0% price growth in July, but this may be due to a lack of suitable properties being available for sale after a year of high demand.

The East Midlands is in second place in Figure 2 above, its highest position in the League since May 2019, with Leicester and Nottinghamshire both experiencing annual price growth in excess of 15.0%. The East Midlands is followed by the West Midlands at 12.9%, with Worcestershire leading the authorities in the region with price growth of 15.8%.

England and Wales Regional Heat Map

There are two distinct groups in England and Wales in July 2022 in terms of house price growth, with eight of the ten GOR areas in England and Wales having rates in excess of 10.0%. The two areas with rates of less than 10% are the South East (8.7%) and Greater London (2.7%).

Transactions

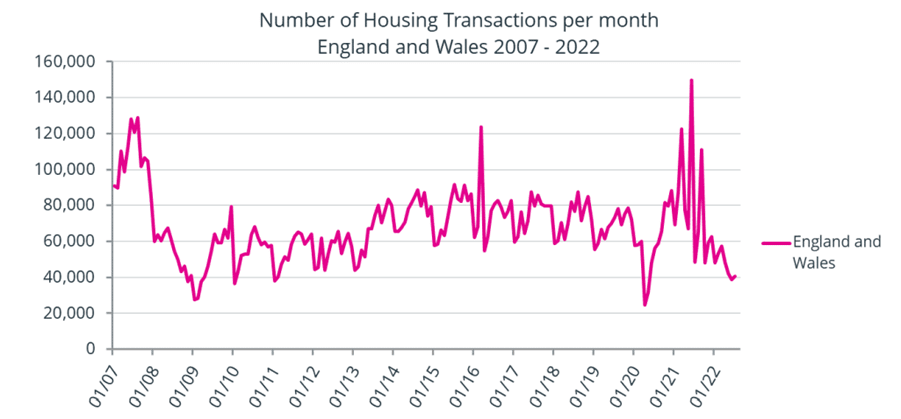

Figure 3. The number of housing transactions per month, January 2007 – July 2022

Figure 3 shows the number of domestic property transactions per month recorded in England and Wales at the Land Registry for the period from January 2007 to July 2022.

As the chart shows, the years 2013 – 2019 were relatively normal, with only the spike in sales in March 2016 – one month ahead of the additional 3% SDLT on second properties – upsetting the usual seasonal patterns that were then prevalent. However, from the start of the pandemic in March 2020, more pronounced changes can be seen in home-buying behaviour, as housing transactions in April 2020 plummeted due to the arrival of the pandemic, to be followed by a slow rise in sales as confidence began to return. Then followed a period when sales exceeded previous levels, from October 2020 to September 2021, as lifestyle changes and the SDLT/LTT tax-holidays resulted in an increase in demand, especially for properties with space to allow for working from home.

Comparing Figure 3 above with Figure 4 on page 8, the impact of the termination dates of the SDLT/LTT tax-holidays and their associated peaks in activity are clearly evident in both transactions and average prices.

Having experienced three tax-related peaks in 2021, transactions from October 2021 through to July 2022 have been running between 40,000 and 60,000 per month. This is below the pre-pandemic norm, at approximately half of the levels seen from January 2017 to December 2019. However, there are currently delays in processing transactions at the Land Registry and it is likely that the gap between the latest months and the pre-pandemic levels will get smaller as further sales are processed by the Land Registry.

Greater London

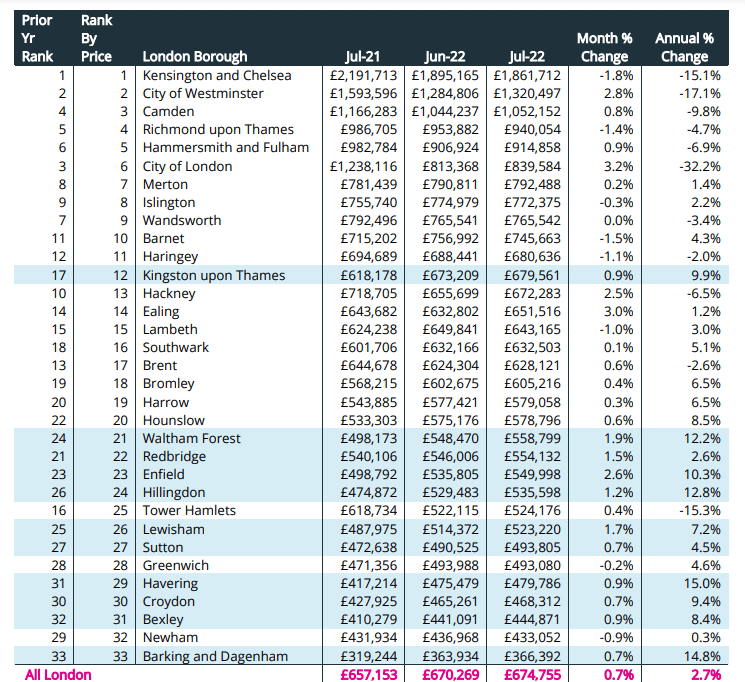

Table 2. The change in house prices, for the 33 London boroughs, comparing July 2021 and June 2022 with July 2022

The analysis of Greater London prices in Table 2 is for July 2022 and compares these prices to one month and one year earlier. It also records the percentage change in these prices over the last month and year. The table is sorted in descending order of the boroughs’ average house prices in July 2022. Boroughs highlighted in blue are currently at a record average price.

There are two main features to be noted from Table 2. Firstly, ten of the eleven boroughs which are currently experiencing record price levels are in the bottom thirteen places by average price, i.e. it is the lowest-priced boroughs that are currently experiencing the highest demand for housing in London – presumably reflecting the extreme affordability pressures that exist in the capital – while the average prices in the six most expensive boroughs are considerably lower than their previous record levels. For example, Camden, which is ranked as the third-most expensive borough in London in July 2022, is some £150,000 short of its highest average price of £1.2 million, which was achieved in June 2019.

Secondly, all six of the six highest-priced boroughs in London are experiencing falling prices in July 2022 compared to twelve months earlier, with only two of the seventeen lowest-priced boroughs having falling prices over the same period (being Brent and Tower Hamlets).

Clearly, in London, there is thus a movement away from the higher-priced areas, especially in the Prime Central Areas, to the more modestly priced areas around the periphery of the Greater London area. It has been suggested that with the hybrid method of working from home for the majority of the week, with only the occasional commute to the office, pied-a-terre and studio flats have become more popular in the central areas of London, with this changing mix lowering the average price of the properties that have been purchased in these boroughs over the last few months.

England and Wales, Greater London and the South East

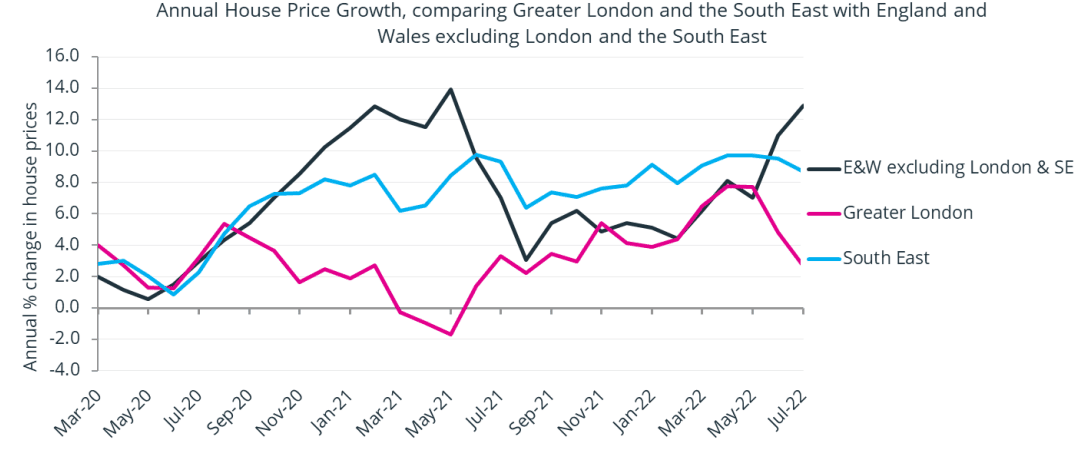

Figure 4. Comparting the annual rates of Greater London and the South East with England and Wales, excluding Greater London and the South East, March 2020 – July 2022

Figure 4 shows the movement in the annual rates of growth of the average house price, with the black line representing England and Wales excluding Greater London and the South East, the red line depicting price movements in Greater London and the blue line showing the price movements in the South East.

All areas saw a decline in their annual rates of growth from March 2020 to June 2020, with prices picking up in July and August 2020, as confidence in the housing market began to return. However, prices in London began to fall from August 2020 through to May 2021, when flats that normally dominate the London market fell out of favour during the pandemic. They had little or no outdoor space in which to live, while ‘working from home where possible’ became a requirement of the Covid restrictions.

Outside London and the South East, prices continued to climb, with peaks being reached in March and June 2021, coinciding with the planned termination of the SDLT tax-holiday in England and the LTT holiday in Wales. In addition, there were ‘lifestyle changes’ affecting the property markets, with purchasers looking for ‘more space’, as well as coastal and rural locations, so to enable life to be potentially more fulfilling, despite the ever-pervasive pandemic discomforts.

The slide in price growth, outside London and the South East, in July and August 2021 (the black line), following the ending of the full rate of tax savings in June 2021, is very distinctive, as is the consequent opposite of this effect twelve months later in July and August 2022.

In general terms, the price increases in the South East have been contained within a growth band of between seven and nine per cent from October 2020 to July 2022, with a few minor exceptions. This is likely to be a consequence of the higher prices prevailing in the South East region compared to the rest of England and Wales, excluding London, with the South East being less influenced by the savings in tax associated with the SDLT tax-holidays.

Finally, we can see the fall in prices in London that have taken place in May to July 2022. Part of this fall will be a consequence of the rise in prices that occurred in London twelve months earlier, and in part will be due to the reduction in the size of flats being bought in the current market – a probable sign of the tightening that is already underway.

Help keep news FREE for our readers

Supporting your local community newspaper/online news outlet is crucial now more than ever. If you believe in independent journalism, then consider making a valuable contribution by making a one-time or monthly donation. We operate in rural areas where providing unbiased news can be challenging. Read More About Supporting The West Wales Chronicle

{kind=link}